Insurance feels like one of those necessary evils, doesn't it? You know you need it, but the process of actually buying it can feel overwhelming. Between the jargon, the fine print, and the sheer number of options, it's tempting to just grab the first policy that sounds decent and call it a day.

But here's the thing: that approach could be costing you big time. Shopping around before buying insurance isn't just a "nice to have" step — it's essential. And I'm not talking about a casual glance at a couple of websites. I mean really digging in, comparing quotes, and understanding what you're actually getting for your money.

Let me walk you through why this matters so much, and more importantly, how to do it right.

The Real Cost of Not Comparing

Here's a scenario that plays out more often than you'd think. Sarah needed car insurance for her new sedan. She went with the first company her parents used because, well, it was familiar. Her premium? $1,800 a year.

Six months later, a coworker mentioned paying just $1,200 for nearly identical coverage. Sarah spent 30 minutes getting quotes from three other insurers. The result? She found comparable coverage for $1,350 — saving herself $450 annually. That's a nice weekend getaway she could've missed out on, just because she didn't shop around.

This isn't an isolated case. According to industry data, consumers who compare multiple insurance quotes typically save between 15% to 30% on their premiums. We're talking real money here — money that could go toward your emergency fund, retirement savings, or that kitchen renovation you've been dreaming about.

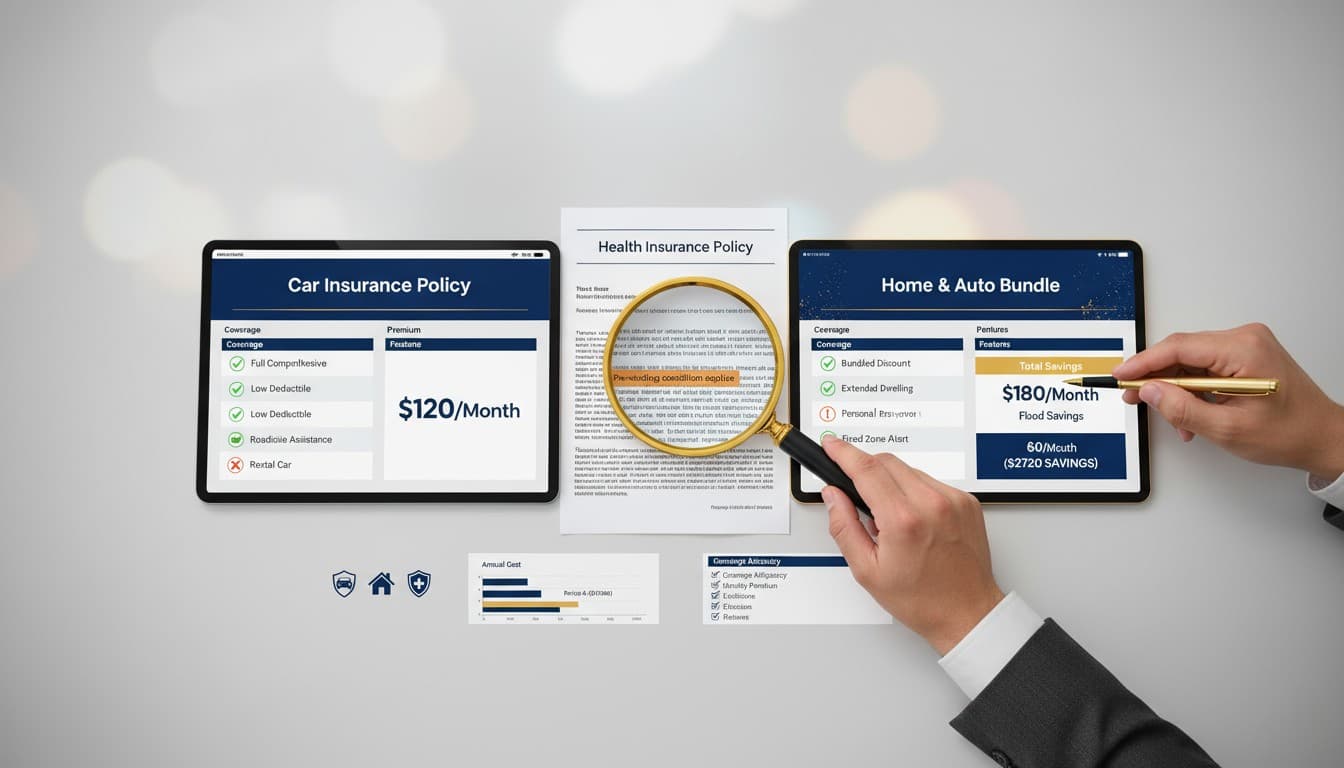

What Actually Changes Between Insurance Companies?

You might be wondering: "Isn't insurance basically the same everywhere?" Not even close. Here's what varies significantly from one provider to another:

Premium prices are the most obvious difference. Two companies can charge wildly different rates for the exact same coverage amount. Why? Each insurer uses its own formula to calculate risk. One company might see you as a higher risk based on your zip code, while another focuses more on your driving record or credit score.

Deductibles and out-of-pocket maximums can make or break your budget when you actually need to file a claim. Company A might offer a $500 deductible with a $150 monthly premium, while Company B offers a $1,000 deductible at $120 per month. Which is better depends on your financial situation and risk tolerance.

Coverage limits are where things get really interesting. Let's say you're shopping for homeowners insurance. One policy might cover up to $300,000 for dwelling protection, while another offers $250,000 at a similar price point. That $50,000 difference could be critical if disaster strikes.

Exclusions and fine print vary dramatically. Some health insurance plans cover mental health services with minimal copays; others treat them as specialty care with higher costs. Some auto policies include roadside assistance and rental car coverage; others charge extra for these features.

The Step-by-Step Guide to Shopping Smart

Alright, let's get practical. Here's how to actually do this comparison shopping thing without losing your mind:

Step 1: Know What You Actually Need

Before you start collecting quotes, get clear on your coverage needs. For car insurance, this means understanding your state's minimum requirements, but also thinking about your specific situation. Do you have a new car that needs comprehensive coverage, or an older vehicle where liability-only might make sense?

For example, Jake drives a 2010 Honda Civic worth about $4,000. Paying $800 a year for comprehensive coverage doesn't make financial sense when the car's total value is so low. He switched to liability-only and saved $500 annually — enough to cover any minor repairs out of pocket.

Step 2: Gather Your Information

Insurance companies will ask for specific details to generate accurate quotes. Have these ready:

- Your personal information (date of birth, address, occupation)

- Vehicle details (make, model, year, VIN) for auto insurance

- Home details (square footage, age, construction type) for homeowners insurance

- Health history and current medications for health insurance

- Current coverage details if you're switching providers

Step 3: Get At Least Three to Five Quotes

This is where the magic happens. Don't just compare two companies — cast a wider net. Include a mix of:

- Big national insurers (they often have competitive rates and extensive resources)

- Regional companies (they sometimes offer better local knowledge and customer service)

- Direct-to-consumer online insurers (they cut out agents, which can mean lower prices)

Use online comparison tools to streamline this process, but also consider calling a few companies directly. Sometimes phone quotes reveal discounts or options not available online.

Step 4: Compare Apples to Apples

This is crucial and where many people go wrong. When you're looking at quotes, make absolutely sure you're comparing identical coverage amounts, deductibles, and policy features.

Maria learned this the hard way. She thought she'd found a great deal on health insurance — $200 less per month than her current plan. But when she read the fine print, she discovered the network didn't include her longtime doctor, and prescription coverage was significantly worse. After adjusting for true equivalent coverage, the "cheaper" plan actually cost more in the long run.

Step 5: Look Beyond the Price Tag

Yes, cost matters, but it's not everything. Research each company's reputation:

Check their financial strength ratings with agencies like AM Best or Standard & Poor's. You want a company that'll actually be around to pay your claims. A financially shaky insurer offering rock-bottom prices is a red flag, not a bargain.

Read customer reviews, but take them with a grain of salt. Focus on patterns rather than individual complaints. If you see consistent mentions of delayed claim processing or unhelpful customer service, that's worth noting.

Look up their claim settlement ratio — the percentage of claims they approve versus deny. This information is often available through state insurance department websites.

Step 6: Ask About Discounts

Insurance companies offer dozens of potential discounts, but they won't always volunteer them. You need to ask. Common ones include:

- Multi-policy discounts (bundling home and auto often saves 15-25%)

- Good student discounts for young drivers

- Safety feature discounts for cars with advanced braking systems or anti-theft devices

- Professional association discounts

- Pay-in-full discounts (paying annually instead of monthly)

- Loyalty discounts (though paradoxically, loyal customers often pay more than new ones)

Tom bundled his home and auto insurance with the same company and added his daughter's car to the family policy. Between the multi-policy discount and multi-car discount, he saved $720 annually — far more than he would've saved by using separate insurers.

Red Flags to Watch For

During your shopping process, be alert for warning signs:

Pressure tactics: Legitimate insurers give you time to decide. If someone's pushing you to "sign today or lose this rate," walk away.

Prices that seem too good to be true: They usually are. Extremely low premiums might indicate inadequate coverage or a company with poor claim-paying practices.

Unclear policy terms: If you can't get straight answers about what's covered and what's not, that's a problem. Insurance is complicated, but your agent or representative should be able to explain things clearly.

When to Re-Shop Your Insurance

Shopping around isn't a one-time event. Life changes, and so do insurance rates. Consider comparing quotes again:

- Annually, even if you're happy with your current provider (loyalty doesn't always pay)

- After major life events (marriage, divorce, buying a home, having kids)

- When your current policy is up for renewal

- If your rates increase without explanation

- After you've made improvements (like installing a security system or paying off your car)

The Bottom Line

Look, I get it. Shopping for insurance isn't anyone's idea of a good time. But here's the reality: spending a few hours comparing options can save you thousands of dollars over the life of your policy. That's a pretty solid return on investment for something that mostly involves clicking around online and making a few phone calls.

The insurance market is competitive, which works in your favor. Companies are constantly adjusting their rates and offerings to attract new customers. By shopping around, you're putting that competition to work for you.

Don't let the process intimidate you. Start with one type of insurance — maybe the one where you suspect you're overpaying. Get three quotes. See what you find. Once you've done it once, you'll realize it's not as daunting as it seemed.

Your future self will thank you when you're not lying awake at night wondering if you're overpaying for coverage you might not even need, or worse, dealing with a claim that reveals you didn't have nearly enough coverage in the first place.

Insurance is about protecting what matters most to you. Taking the time to shop around ensures you're doing that smartly, efficiently, and without throwing away money that could be working harder for you elsewhere. That's not just good insurance sense — it's good life sense.